Nigeria stands out as one of the most expensive property markets globally, ranking second in Africa after Angola. The high costs are not solely due to construction expenses but are influenced by various other factors. These include the high cost of borrowing funds, fees imposed by government agencies, and market uncertainties affecting property turnover.

In an interview with BusinessDay, a developer highlighted that these factors significantly inflate house prices, surpassing construction costs by nearly 40 percent. "Finance plays a crucial role; constructing a property under N10 million is challenging due to the high cost of funding," he explained. "When seeking $2 million for a project, the financing costs escalate, driving up construction expenses."

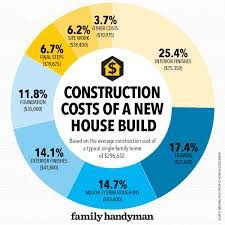

The developer emphasized that although the actual construction cost of a house may be less than N25 million, factors like interest rates, which can add up to N5 million, and government charges contribute to selling prices reaching N40 million. "With a stable market and accessible financing, even a N3 million profit per house would suffice, but uncertainties and high finance costs necessitate higher pricing," he reasoned.

Nigeria has faced a housing deficit of over 17 million units for more than a decade, exacerbated by a population growth rate outpacing economic expansion since 2015. The Association of Housing Corporation of Nigeria (AHCN) highlights the underdevelopment of the mortgage industry, where over 90 percent of new homes rely on personal savings for construction.

Developers continually seek alternative funding sources, as traditional bank credit remains inaccessible and unaffordable due to high interest rates and short-term deposit nature. Commercial banks, unsuitable for long-term real estate projects, subject developers to economic fluctuations like interest rate changes, exchange rate variations, and inflation rates.

Despite a slight recovery with 0.93 percent growth in the first quarter of 2019, after 12 consecutive quarters of decline, the real estate sector faces dwindling bank credit confidence. Credit allocation to real estate plummeted to 3.92 percent, its lowest in four years, out of N15.21 trillion total credit disbursed across 17 sectors by deposit money banks in early 2019.

Comparatively, in South Africa, where mortgages account for nearly 30 percent of total credit, the real estate sector's stability contrasts sharply with Nigeria's challenges. South African banks hold assets valued at approximately ZAR5.14 trillion ($382 billion), demonstrating the significant disparity in mortgage financing between the two countries.

- Cost Factors: Apart from construction costs, other expenses such as high interest rates, government charges, and market uncertainties play significant roles. These factors can increase property prices by up to 40%.

- Impact of Finance: Developers cite financing as a major challenge. The high cost of borrowing money affects construction costs, forcing developers to sell properties at higher prices to cover expenses.

- Market Dynamics: Unlike predictable markets, Nigeria's property market faces uncertainty. Developers must account for potential delays in selling properties, which influences pricing strategies.

- Housing Deficit: Nigeria has a shortage of over 17 million housing units. This deficit continues to grow due to rapid population growth, outpacing economic development.

- Challenges in Mortgage Industry: The underdeveloped mortgage sector limits access to affordable financing. Most new homes rely on personal savings for construction, hindering widespread homeownership.

- Banking Sector Limitations: Commercial banks offer short-term deposits unsuitable for long-term real estate projects. This mismatch, combined with economic fluctuations, affects credit availability and interest rates.

Despite recent growth in the real estate sector, challenges persist. Banks remain cautious about lending to real estate, impacting sector growth and affordability.

{kind=link}